Motor Loan vs Personal Loan: Best Way to Buy a Bike in Malaysia

Everyday, people are always out and about, be it for work or for pleasure. People always move and transport from places to places. Transportation like car and motorbike has become a necessity. A decision to buy a vehicle, be it a car or a motorbike can be influenced by various factor like cost, comfort, preference and maintenance.

With the cost of owning a car in Malaysia is rapidly increasing, many people has turned to buying a motorbike as an option; be it via motorcycle loan or cash. Eventhough some people can still afford to buy used car, it is still a huge monthly commitment that people have to payback.

Process of Hire Purchase Loan- Motorcycle Loan

The process of buying a motorcycle surely is brief compared to the process of buying and owning a used car or a brand new car. Not only that, transporting using a motorbike save a lot of time, and it also help save the maintenance cost, gas, as well as insurance cost as it is a lot cheaper. Compared to car’s monthly instalment, you can buy a motorbike with an instalment as low as RM100 per month, depending on the payment type.

There are two types of payment that you can choose from, which are via motorcycle loan or full on cash by making a personal loan. Hence, it is not an unfamiliar scene to see people getting a personal loan to purchase a used motorbike with high capacity like superbike as they successfully obtain an affordable monthly instalment.

Here, we will help you compare which type of motorbike purchase type is more suitable for you, Motorcycle loan vs full cash (personal loan).

Table of contents

- Process of Hire Purchase Loan- Motorcycle Loan

- Hire Purchase Financing

- Personal Financing– Alternative of Motorcycle Loan?

- Advantages of Personal Loan

- Comparing Motorcycle Loan vs Personal Loan

- Infographic: List of Cheapest Motorbike in Malaysia

- 4 Major Mistakes to Avoid When Buying a Motorcycle via Shop Loan

- Conclusion

Hire Purchase Financing

The conventional financing mode for motorcycle purchase is via motorbike loan due to its lease-to-own scheme. Consumers are able to utilise the vehicle while paying installments, although they do not gain ownership until the full amount has been paid. Interest (or profit rates under Islamic banking) and tenures may differ depending on the type of motorcycle purchased.

Despite that, This financing mode will charge high interest rate (or better known as profit rate) in islamic banking like personal and koperasi loan, and the pay back period depends on the type of motorbike that you want. Normally, customer are more fond of motorcycle loan purchase from supplier as they will be offered cheap instalment, with a long payback period. There are also some customers that would prefer a shorter period of payback as it is faster.

One of the most favoured motorcycle loan is AEON Credit Motorbike loan when it comes to buying motorbike. This is because most of motorcycle shop in Malaysia provide motorcycle loan using AEON credit. This hire purchase motorcycle loan makes everything easier for the borrower to get the motorbike that they desire as AEON is a syariah compliance and lenient passing criteria. The rate that is offered are also affordable.

Below is a typical financing package offered under the AEON Credit Motorbike loan (the information disclosed is accurate during the period it was written).

| Type of Motorcycle |

Interest/ |

Maximum Tenure | Margin of Finance |

| Moped (under 250cc) | From 0.833% | New: Up to 60 months Used: Up to 48 months |

Up to 90% |

| Big Bike, Superbike & Maxi Scooter (250 cc & above) | From 0.375% | 12 – 84 months (for both new and used motorcycles) | Up to 90% |

| E-Bike (electronic motorcycle) | From 0.65% | Up to 48 months |

Up to 90% |

*information is accurate when the article is written

Personal Financing– Alternative of Motorcycle Loan?

Meanwhile, an alternative financing channel for your motorcycle purchase is through personal loan, whereby consumers borrow the required funds from financial institutions and pay installments for the personal loan instead.

Advantages of Personal Loan

- Full ownership of the motorcycle (purchased through cash from dealer)

- Longer maximum tenure can be up to 120 months

- Lower monthly installments (loan distributed over a longer period of time)

Nevertheless, a caveat of personal loan financing is its dependency on the consumer’s personal credit history like CCRIS & CTOS and loan eligibility. Applicants opting for personal financing are subjected to credit checks and stringent requirements, in addition to a potentially long wait for funds.

For example, Co-op Bank Pertama offers a personal loan with a promotional interest rate as low as 2.95%.

Comparing Motorcycle Loan vs Personal Loan

Here we use 2 examples – a new under 250cc bike and another new under 650cc superbike using motorbike financing (from AEON Credit) and personal financing (from Public Islamic Bank) to compare which one is more worth it and cheaper. The personal loan from Bank and Koperasi Public Islamic Bank (MCCM) is only offered to government worker with interest rate of 3.99% per annum, and 0.33% per month.

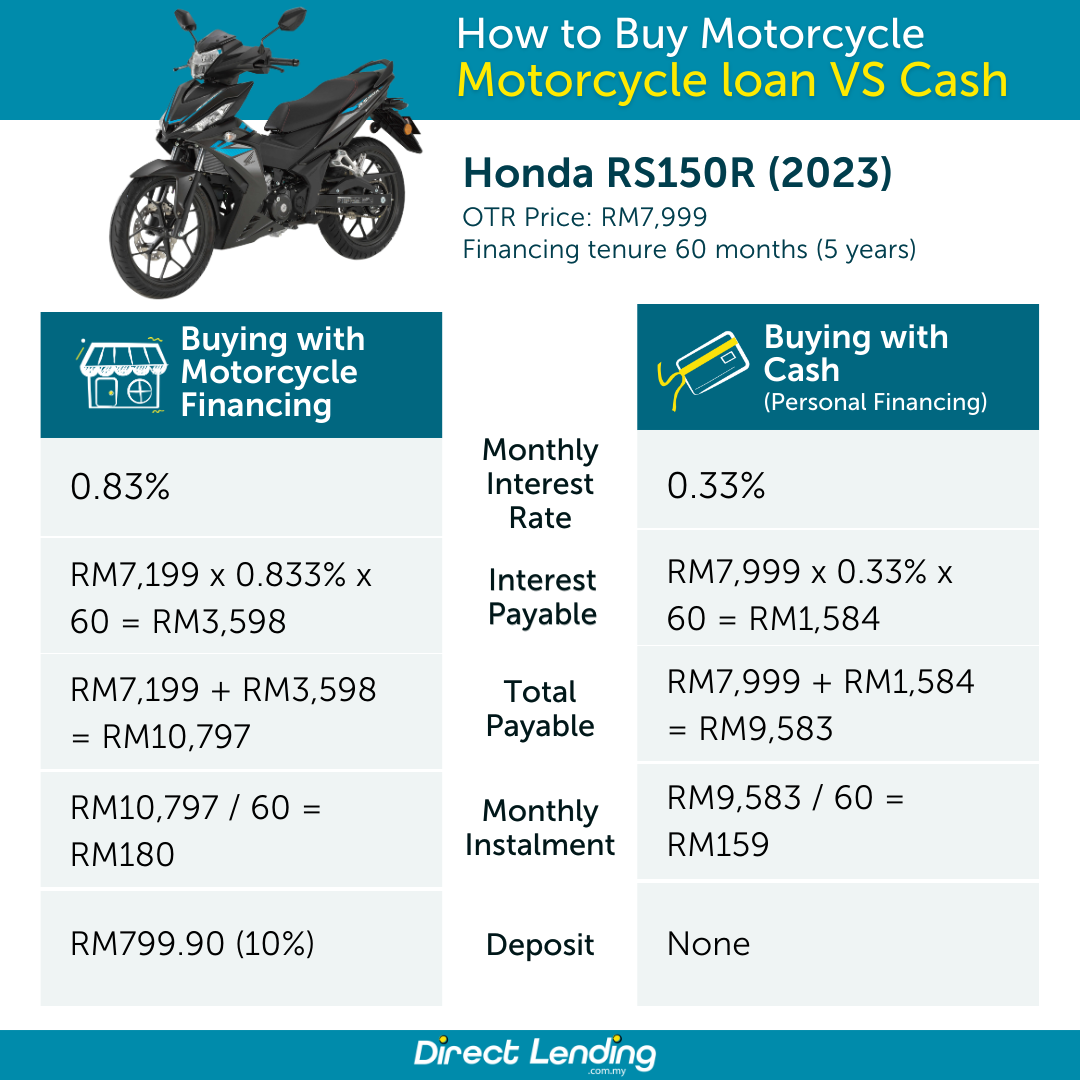

Example 1: Purchasing a Honda RS150R Motorcycle (2023) 149.2cc with on the road price at RM7,999

| Motorbike Loan | Personal Loan | |

| Monthly Profit Rate | 0.83% | 0.33%** |

| Tenure | 60 months | 60 months |

| Interest Payable | RM7,199 x 0.833% x 60 = RM3,598 | RM7,999 x 0.33% x 60 = RM1,584 |

| Total Payable | RM7,199 + RM3,598 = RM10,797 | RM7,999 + RM1,584 = RM9,583 |

| Monthly Instalment | RM10,797 / 60 = RM180 | RM9,583 / 60 = RM159 |

| Deposit Payment | RM799.90 (10%) |

No |

**This is an estimation of the monthly profit rate. The promotional rate and the approved rate would depend on the credit profile and history of the borrower.

In this case, the consumer saves almost RM2,000 from the interest amount by financing the purchase of this bike through a personal loan, with a lower monthly installment per month. Moreover, no deposit payment needed with this purchasing method.

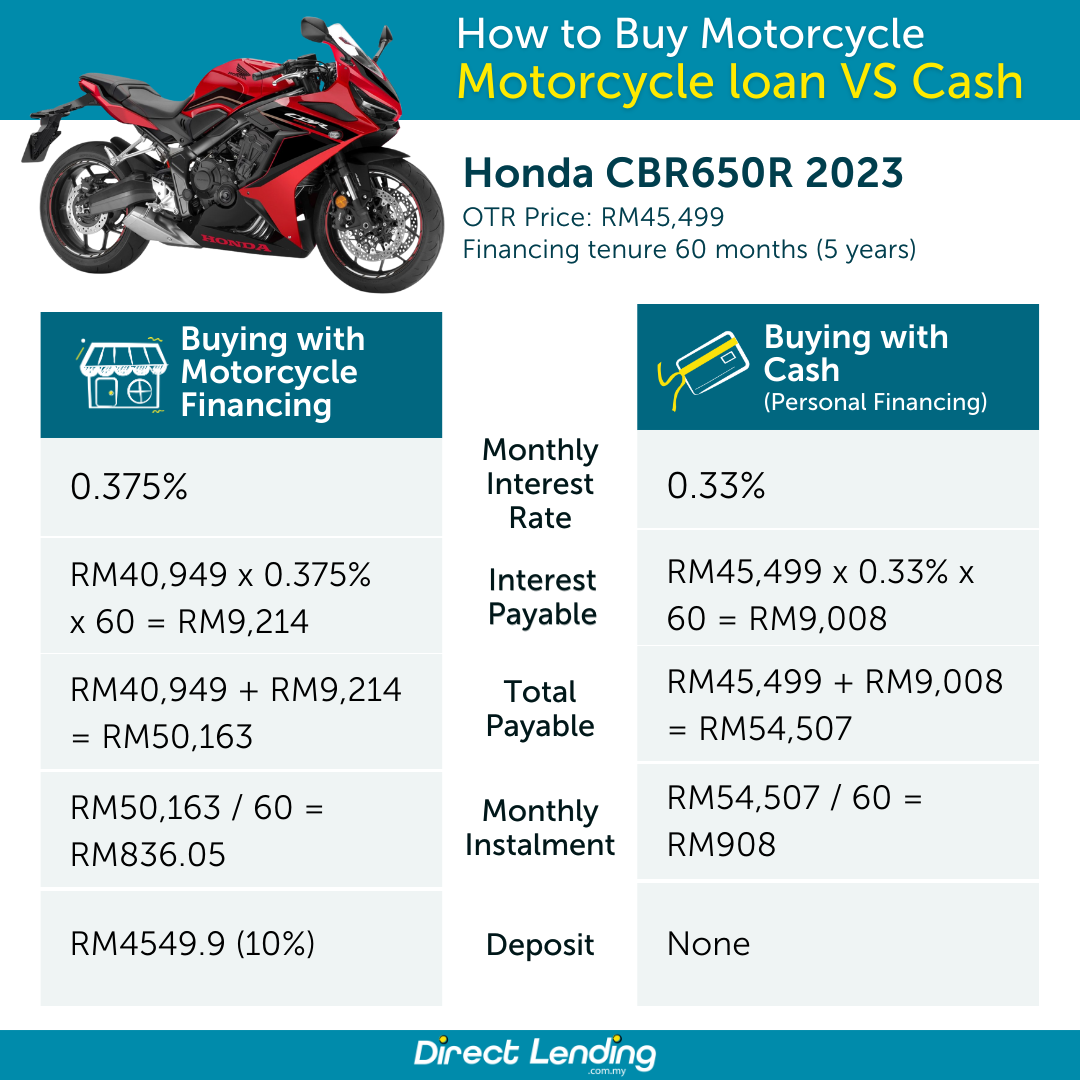

Example 2: Purchasing a Honda CBR650R Motorcycle (2023) 649cc with on the road price at RM45,499

| Motorbike Loan | Personal Loan | |

| Monthly Profit Rate | 0.375% | 0.33%** |

| Tenure | 60 months | 60 months |

| Interest Payable | RM40,949 x 0.375% x 60 = RM9,214 | RM45,499 x 0.33% x 60 = RM9,008 |

| Total Payable | RM40,949 + RM9,214 = RM50,163 | RM45,499 + RM9,008 = RM54,507 |

| Monthly Instalment | RM50,163 / 60 = RM836 | RM54,507 / 60 = RM908 |

| Deposit Payment | RM4,549.90 (10%) | No |

**This is an estimation of the monthly profit rate. The promotional rate and the approved rate would depend on the credit profile and history of the borrower.

In this case, customers do not have to fork out RM4,000 just to pay upfront for the high deposit. Do take note that some motorcycle store may request even higher upfront payment with 20% deposit.

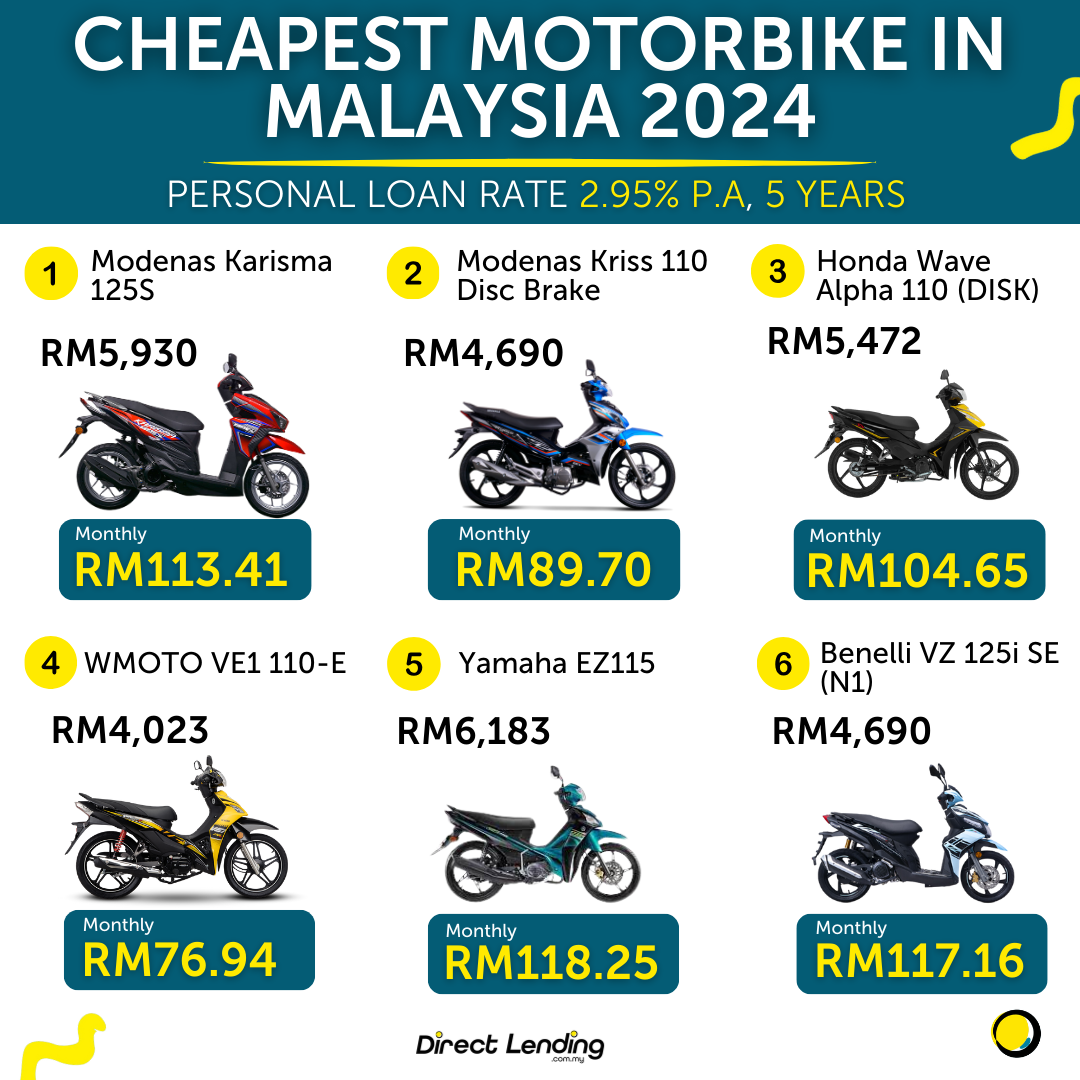

Infographic: List of Cheapest Motorbike in Malaysia

4 Major Mistakes to Avoid When Buying a Motorcycle via Shop Loan

Many buyers get easily excited when they see promotional ads flashing cheap monthly installments on social media. However, if you do not carefully scrutinize the agreement structure of a motorcycle, you risk paying a total price that is significantly higher than the actual value of the motorcycle.

Before you step into any showroom to buy a motorcycle with a motor loan, make sure you avoid these common pitfalls to protect your wallet:

1. Falling for the "RM0 Down Payment" Tactic

"Zero down payment" or "muka kosong" deals sound incredibly tempting, especially if you are tight on upfront cash. But in the financing world, the rule is simple: the lower your down payment, the higher the principal loan amount subjected to interest. Consequently, the total interest snowballs, forcing you to bear high monthly installments over a long period.

💡 Direct Lending Tip: If your budget is tight but you want to avoid the high interest rates of a shop loan, a great alternative is applying for a personal loan through Direct Lending. You can secure the full cash amount to buy the bike outright, skip the headache of a 10% deposit, and the motorcycle becomes 100% yours from day one.

2. Not Verifying the Actual Interest Rate (Flat Rate vs. Effective Rate)

Credit companies tied to a motor loan kedai usually advertise a monthly flat rate, such as 0.833% per month. It sounds minimal, right? However, when converted into an actual annual interest rate, it can easily skyrocket to 10% to 12% per annum!

In contrast, the bank and co-operative personal loans for government workers offered on Direct Lending feature interest rates that are far more transparent and competitive. Always ask the dealer to print out a full amortization schedule before you agree to sign any documents.

3. Overlooking Hidden On-The-Road (OTR) Costs

When learning the actual way to buy a new motorcycle, the price tag you see on the catalog brochure is rarely the final price you pay. You need to verify whether the shop's loan package already includes JPJ registration fees, shop processing fees (runner fees), and motorcycle insurance premiums. If you lack the cash to cover these initial side costs, a flexible personal loan can help bridge these hidden expenses without touching your emergency savings.

4. Opting for an Overly Long Loan Tenure (Up to 7 Years)

Stretching your loan tenure to 5 or 7 years will indeed shrink your monthly payments (sometimes down to just RM100 a month). However, by the fifth year, your motorcycle’s market value will have depreciated heavily, yet you will still be stuck paying off interest to the shop. Ideally, keep your motorcycle loan tenure within a sweet spot of 3 to 4 years max.

Conclusion

Is personal loan a better option to finance your motorcycle purchase in Malaysia? It might be, from the perspective of a lower monthly repayment. The answer will also depend on your own credit profile and your access to credit. As a smart consumer, you should assess all possible options before deciding on the facility that suits your financing needs. Try exploring different personal financing options. It might be well worth the time.

This article is written by Direct Lending – An online personal lending platform that provides bank and koperasi personal loan as well as licensed moneylenders personal loan. We can help you find, compare and apply personal loan that best suits your financial needs. Check your eligibility for free, no upfront payment or processing fees and get a loan rates from 2.82% p.a. or 2 working days.

(This article was originally published on the 13th of February 2018 and updated on the 19th of May 2026).

Enjoy reading articles like this? Follow us on our Facebook

page & blog for more tips on personal finance.

{kind=link}

{kind=link}

{kind=link}