10 Best Ways To Pay Off Car Loan Faster

According to a survey done by Rakuten Insight in 2019, 61% of the Malaysia population owns a car. As of 2020 April, there were 31.2 million units of cars registered, while the Malaysia population is 31.9 million. This means some households own more than one car. It is no surprise that an auto loan is one of the biggest financial obligations we can have. Here are 10 ways to pay off car loan faster and help you get an early settlement car loan. If you are in short of fund but need to get your car fix, check out our car repair instalment plan for emergency aid.

Table of contents

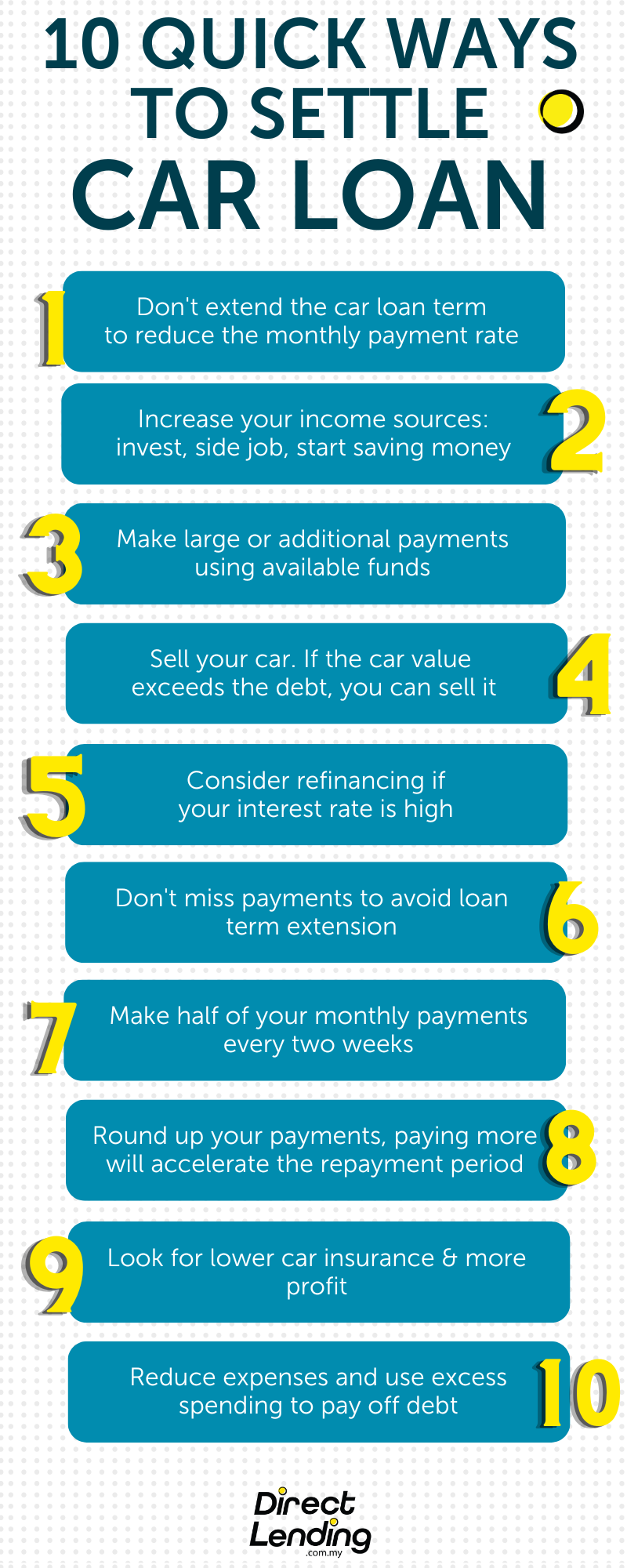

- 1. Don’t Extend Your Term Just For Lower Monthly Payments

- 2. Increase Your Source Of Fund

- 3. Make A Large Payment A Year

- 4. Sell Your Car

- 5. Consider Refinancing Your Current Car Loan

- 6. Never Skip Payments

- 7. Round Up

- 8. Pay Half Your Monthly Payment Every Two Weeks

- 9. Looks For A Cheaper Car Insurance Rate

- 10. Cut Expenses

- Summary

1. Don’t Extend Your Term Just For Lower Monthly Payments

Before we go into how we can pay off loans faster, you should start with choosing the right car loan for yourself. More often than not, people take out car loans to purchase cars they can’t afford. The car salesperson will tell you that you can afford the brand-new Honda Civic that costs RM140k with your RM4k salary. 9-year tenure with a 4% interest rate, you just have to pay RM1,762 a month, which leaves you RM2,238 for other expenses.

If you don’t have many other commitments, you would think it is affordable. But if you do the math, you will be paying RM190k in total, including a RM50k interest when you could’ve used the 50k to purchase a Myvi. Why pay so much interest for something that will depreciate after 9 years? The resell value would be much lower than the original price of the car by the time you finish paying off your loan. So, remember, don’t always extend your term just to lower your monthly payment.

2. Increase Your Source Of Fund

Easier said than done, but these are the ways that could help you increase your monthly income or savings.

(i) Get a side gig – another effective way of bringing in extra income. These are the jobs that don’t require a lot of commitment, such as part-time cashiers/waiters, tutoring, delivery drivers, freelancing, or selling things online. You can find a side job that best suits your interests and skills. This way, even when you have to work during your off days, it won’t feel draining but productive.

(ii) Start investing – investment is a type of passive income, which means income that still comes in automatically even when you’re not doing anything. All you have to do is do some research, put in the money, and you will be getting the interest returns monthly/annually. There are many low-risk investments in Malaysia, you can read more in our other article (can link to the tips of managing personal finance article)

(iii) Start saving money – save at least 20% of your income every month. Transfer the fund into another account, hide it under your bed, and do whatever it takes to save them. Once you have saved enough, you can do an early settlement for the car loan. Besides, the money can be used as an emergency fund. If something happens and you need to spend more than planned, it won’t disrupt your budget or expenses for the month. You can open savings accounts that have a high-interest rate.

3. Make A Large Payment A Year

Making a large payment once in a while can reduce your balance rapidly. Utilize your tax refunds, bonuses, and pay raises. Whenever you receive a large amount of money, use it to pay back your car loan. Don’t spend it unnecessarily, you will thank yourself after.

4. Sell Your Car

Sell your car for a more affordable alternative – if you are having trouble paying back your car loan because it’s just too much, you can always sell it and buy a cheaper one. However, you need to weigh the pros and cons and calculate whether it is worth it or not before you do that.

Cars depreciate fast. If your car is worth more than you owe, means you can sell it and get a big enough amount to purchase a cheaper liable car. If you owe more than what your car is worth, it isn’t really a smart move to sell it and buy a cheaper car because then your car would’ve worth so less, there isn’t much money you can use to buy a new car.

5. Consider Refinancing Your Current Car Loan

If your current car loan has a high interest rate, choosing to refinance may bring you more benefits. You could save so much more or you could shorten the tenures. If you now have a better credit score and are eligible for loans with a lower interest rate and better conditions, why not? However, you should weigh the pros and cons and consult a loan consultant on whether you should refinance or not. If you have paid off most of the car loan, then it’s no longer worth it to refinance to a cheaper loan.

6. Never Skip Payments

Some lenders will let you skip your payment once or even twice a year. Resist the temptation. Skipping payments will lengthen the term of your loan and cost you more in interest.

7. Round Up

Instead of just paying what is recommended, make an extra monthly payment on the amount of your current auto loan rounded up. to help repay your car loan more quickly.

For example, if you borrowed RM140,000 at a 4% interest rate for 9-years tenure, then your monthly payment is RM1,762. With that payment, you’ll repay your car loan in 108 months, having paid RM50k in interest.

However, if you decide to round up and pay RM2,000 a month, you’ll repay your car loan in 7 years and 6 months, having paid only RM44.8k in interest — saving you RM5.2k!

8. Pay Half Your Monthly Payment Every Two Weeks

If you can’t afford to pay extra, consider paying more frequently. There are 12 months in a year, but 26 fortnights in a year. If your loan is set up with monthly payments, split them in half and make payments every two weeks, you’ll make the equivalent of 13 monthly payments in a year, and that’s an extra month’s repayment. If you do this over time, you may be able to reduce the amount of time you are in debt.

Another advantage of increasing your payment frequency is that you may pay less interest over the lifetime of the loan. Paying every two weeks means your loan balance is constantly decreasing, which means you’ll pay less interest on your remaining balance versus paying once a month.

However, check with the dealer about your loan because some lenders only accept exact monthly repayments, so it may not apply to some cases. Additionally, not all lenders will allow you to make extra payments.

9. Looks For A Cheaper Car Insurance Rate

It’s time to evaluate your coverage and get offers from different agents if you haven’t browsed around for lower car insurance over the last few years.

If you’re satisfied with your present insurance provider, talk to your agent about different options for lowering your car cost of insurance. Explore all possible discounts and consider increasing your deductibles and/or reducing your coverage. Keep in mind that while adjusting those criteria will lower your premium, you will need to pay extra costs if an accident occurs.

Get quotes from two or three other insurance companies. To simplify the comparison shopping, try to get rates on the same coverage from each company.

10. Cut Expenses

Cutting off other monthly budget expenditures for a while also means having income that you can use towards your car payment. When you find a way to lower a fixed expense, apply that same amount to your car loan payment each month. Perhaps you cut memberships completely to the gym, subscription boxes, or other monthly membership services. Put those monthly fees toward your loan. Read more on how to pay your loans effectively.

Summary

Figuring out how to pay off a car loan faster depends largely on your financial situation. Finding extra money to put toward the loan can help you eliminate that debt faster.

This article is written by Direct Lending – An online personal lending platform that provides bank and koperasi personal loan as well as licensed moneylenders personal loan. We can help you find, compare and apply personal loan that best suits your financial needs. Check your eligibility for free, no upfront payment or processing fees and get a loan rates from 2.95% p.a. or 2 working days.

{kind=link}