5 Tips To Get Your Personal Loan Approved Faster

Are you currently short on funds and thinking of applying for a personal loan, but not sure how to? Or you have apply and wonder how does your personal loan approved? Well, worry no more! In this article, we have put together a few steps you can take in increasing the chances of your loan applications getting fast approval by bank and non-bank.

Table of contents

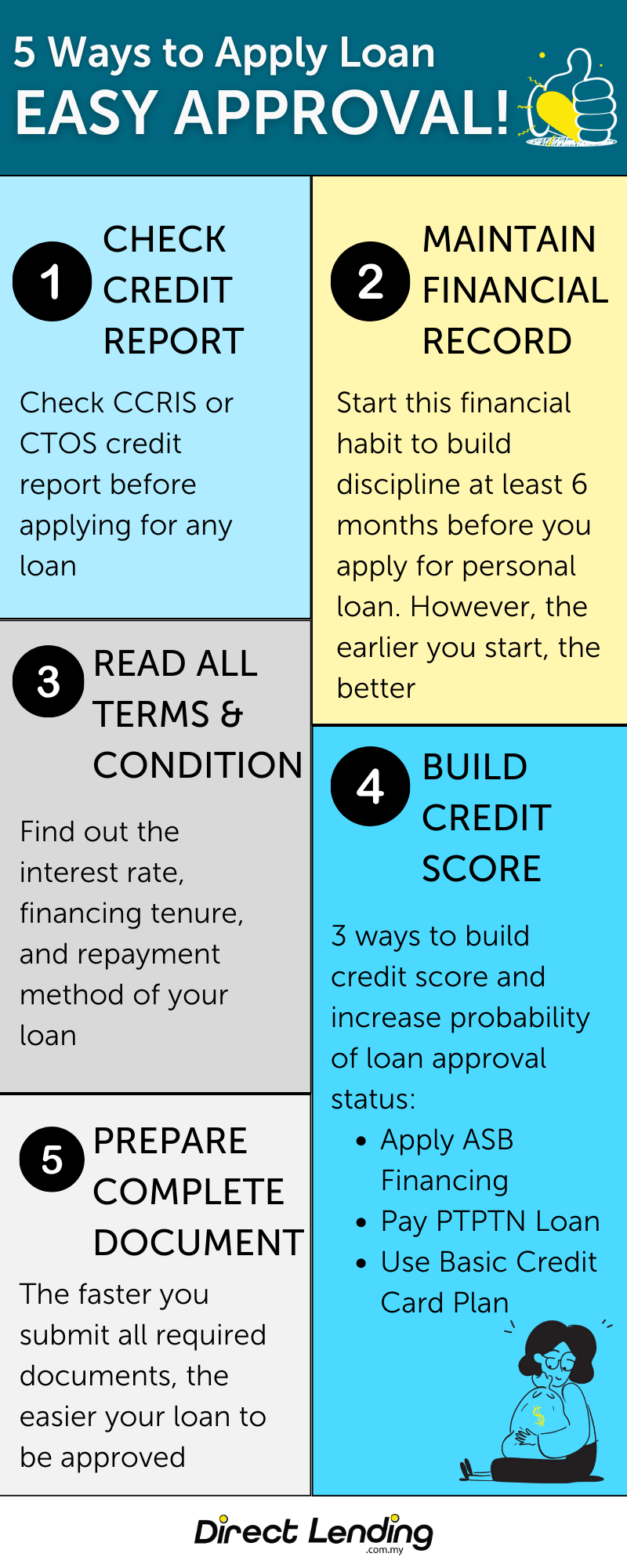

- 1. Check Your Financial Records

- 2. Be Discipline

- 3. Read All Terms & Conditions

- 4. Start Having A Credit Record

- 5. Prepare the Required Documents

- Infographic: Tips to Apply for Fast Approval Loan

- Alternatives to Personal Loans Besides Conventional Banks

- Video: Tips to Apply Loan to Avoid Getting Rejected

- Conclusion

1. Check Your Financial Records

If you are applying for a loan or a credit card, you should know your own credit score. Having a low credit score may cause your loan to be charged with a high interest or your application might be rejected altogether.

Your credit record is reported in CCRIS (Central Credit Reference Information System), which is managed by the Central Bank of Malaysia (BNM), and it can also be obtained from other credit reporting agencies (CRA) such as CTOS and Experian. You can get CCRIS & CTOS report for free from Bank Negara and private company.

Basically, a credit record is a statement of your credit history which includes banks or credit agencies that provided you with credit or loans. The information on your past repayment behaviour that can be accessed by CCRIS and other credit reporting agencies is derived from sources including your past personal loans, mortgages, car loans, credit cards and PTPTN student loans.

If you have ever failed to make repayments on loans or credit cards, or have not paid on time, it will be recorded in your credit report. If you have any legal actions taken upon you with regards to your loan repayments, it will also be recorded.

To add to that, even late repayments on utilities like your telephone bills can also lead to a bad credit record and thus making it difficult for you to obtain approval on a loan.

In ensuring that your credit score is good, your credit record should be clean and free from history of late repayments and defaults. This will then help banks to make good assessments of your profile and thus making it easy for your loan applications to be approved.

2. Be Discipline

In order to have a clean financial record by the time you start applying for a loan, you should begin to maintain a good discipline in paying your existing loans and bill payments about six months prior. Having said that, it is never too early to start being disciplined financially.

Even if you do not intend on making any loan application in the near future, paying your financial commitments on time is always the best option to ensure that your credit score is always maintained well.

This is especially useful if you ever need to have a loan application approved quickly, such as when applying a personal loan to cover healthcare costs. Again, always be disciplined if you want loans to be approved easily.

3. Read All Terms & Conditions

It is crucial to read and understand all terms and conditions set by a financial institution before applying for any loan.

Some of the eligibility requirements that should be given attention to before applying are minimum salary limits, age limits, and maximum loan amounts. Do thorough surveys of each potential creditor’s terms and conditions so that you can avoid wasting time applying for loans that you are not eligible for.

Another point to note is that banks will usually only approve a personal loan if the repayment amount is not more than 30% of your other existing financial commitments.

For a personal loan, banks will approve a loan amounting to 2 or 3 times your income. Therefore, calculate your total financial commitment and have an understanding of the bank’s terms and conditions.

4. Start Having A Credit Record

Some banks refuse to lend out money to individuals who do not have any prior credit record at all, particularly those who do not own any existing financial commitments like mortgage loans, car loans, or credit cards.

This is because these individuals have no written proof of their past behaviour with loan repayments, even if they have always been disciplined with all their payments. Banks, on the other hand, are unable to assess these individuals’ abilities to repay the loan that they have applied for.

Therefore, it is advisable for you to take up a financial commitment (if you do not yet have any) so that you can gain a credit record, making it easier for banks to assess your repayment abilities and have your loan approved.

One way to start is by signing up for a credit card from your preferred financial institution and start using it for your regular transactions. By doing this, you can also benefit from the rebates, cashbacks, and discounts offered by merchants.

Nevertheless, you should remember that taking up a new commitment, such as a credit card, comes with the responsibility of using it wisely and paying bills with discipline. This is to ensure that not only do you start having a credit record, but you also maintain a good credit score.

5. Prepare the Required Documents

Infographic: Tips to Apply for Fast Approval Loan

Alternatives to Personal Loans Besides Conventional Banks

So, what will happen if you do not meet the eligibility requirements to apply for a loan from the bank? Actually, there are several safe and legal financing options aside from applying for a bank loan, such as cooperative loans and licensed moneylender loans.

These alternative financing options can assist you in financial emergencies or for any purchases, such as buying a used car that is over 5 years old or a car valued below RM10,000, as most banks will not approve hire-purchase loan applications for such vehicles.

Koperasi Loans and Licensed Money Lenders

Cooperative loan (often known as Koperasi Loan) is a type of personal loan that is offered to civil servants working with the federal and state level governments, local authorities, statutory bodies and selected government agencies. Usually, cooperative loan repayments are made through automatic salary deductions on ANGKASA. Most cooperative loans offered are Shariah-compliant.

Among those offering loans to civil servants are koperasi that are registered under the 1993 Cooperative Act, these include Koperasi Coopbank Pertama, Koperasi Ukhwah, Koperasi Putri Terbilang (KOPUTRI) and Koperasi Bersatu Tenaga Malaysia Berhad (KOBETA).

Besides koperasi, certain foundations (also known as Yayasan) offer personal loans to civil servants. Among them are Yayasan Ihsan Rakyat and Yayasan Dewan Perniagaan Melayu Perlis. Although these institutions are not similar in nature, the financial products that they offer are, including their preferred repayment method which is through salary deductions via ANGKASA.

Last but not least, some banks in Malaysia have partnered with local entities (e.g. Public Bank-MCCM Resources, Ambank-MCCM Resources) in offering personal loans with similar repayment schemes to cooperatives, i.e. through salary deductions via ANGKASA.

Licensed Money Lenders

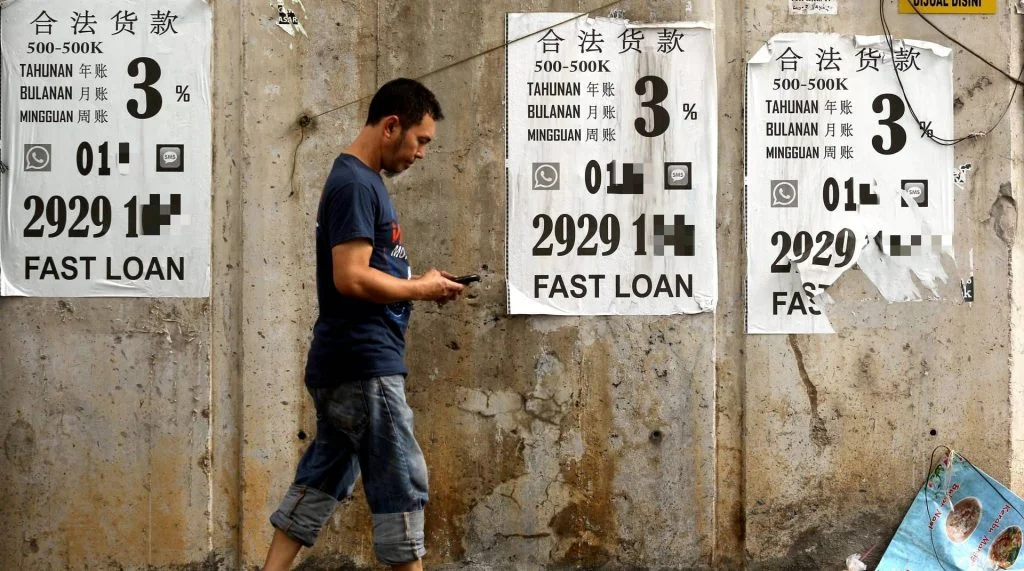

Meanwhile, licensed moneylenders are governed by the Ministry of Local housing and Government (KPKT) and regulated under the Moneylenders Act 1951. This regulation means that the licensed moneylenders are prevented from charging exorbitant interest rates and free to set their own terms and conditions, unlike ‘Ah Long’ (or also known as loan sharks). While the former can charge only up to 12% interest rate, the latter can charge up to 30% interest rate!

If you are still unsure, you can refer to KPKT’s official website for more information on licensed moneylenders or credit community companies, and any complaints or enquiries can also be lodged on the website.

Avoid Ah Longs At All Costs

Many have jumped to the conclusion that all licensed moneylenders equate to Ah Long, when this is not true. In contrast, there are certified and licensed money lenders, more formally known as credit communities, that are regulated by KPKT.

KPKT recently launched an initiative to rebrand registered licensed moneylenders as the ‘Credit Community’ with the purpose of changing the general public’s perception and exposure towards safe lending facilities, as this is a challenging time whereby many individuals are stuck with financial difficulties.

How to Identify Personal Loan from Ah Long?

1. Check the potential moneylender’s company SSM number through the i-KrediKom application on KPKT’s official website.

i-KrediKom is a free application for the public to search for licensed credit community firms in Peninsular Malaysia, file complaints, and obtain information as per written in the Moneylenders Act 1951.

2. Check the availability of a business operating license. If it is readily displayed in their business premise, ensure that the license is issued by KPKT, and not BNM.

3. Make sure that the potential moneylender abides by regulations stated in the Moneylenders Act 1951, i.e. charges an annual interest rate of not more than 18% and uses proper written contracts in their transactions.

Video: Tips to Apply Loan to Avoid Getting Rejected

Conclusion

Now that you have learned what influences a bank’s decision whether to approve a loan application or otherwise, you no longer need to worry too much about your loan application. Each bank will assess clients in their unique ways, but the basic step that each client has to take is providing banks with the necessary information, specifically on the credit record.

We hope that the information that has been shared will help you to understand better what needs to be done to get an increased loan approval rate in the future.

This article is prepared by Direct Lending, an online personal lending platform that offers bank & koperasi personal loans, especially for the civil servant. We help can help you to find, compare and apply financing that best suit your financial needs.

{kind=link}

{kind=link}

{kind=link}