Impact of Base Rate (BR) & Revised Reference Rate Towards Your Loan

History Of The Reference Rate Framework

The Reference Rate Framework was introduced in 1983, where the Base Lending Rate (BLR) was used as the reference rate for retail floating-rate loans. Since then, the provision and implementation for the Base Lending Rate have grown in line with the development of the financial sector.

However, the Base Lending Rate is deemed to be less relevant as a Reference Rate as it is less transparent and has made it more difficult for borrowers to make the right decisions for retail floating-rate loans. On the 2nd of January 2015, the new Reference Rate Framework was implemented to replace the older version with the intent of providing a more transparent Reference Rate to the borrowers. The Base Lending Rate was replaced by Base Rate (BR) to aid borrowers in making a more accurate decision when choosing financial products such personal loan offered by financial institutions. The financial institutions were given the freedom to determine their own Base Rate.

Table of contents

- History Of The Reference Rate Framework

- What is a Reference Rate?

- The OPR Rises Again! Should You Apply For Fixed Or Floating Rate Loan?

- What is the Revised Reference Rate Framework? What are the differences?

- Understanding The Impact Of Transitioning From Base Rate To Standardised Base Rate

- The Differences between Standardised Base Rate, Base Rate and Base Lending Rate

- Direct Lending’s Opinion

- What do you need to do if you want to apply for retail floating-rate loan starting 1st August 2022?

What is a Reference Rate?

You might be wondering “What are retail floating-rate loans?” “Why are there multiple types of Reference Rate?”

Retail loans are loans for individuals, meaning it is not a business loan or small and medium enterprise loan. While the floating-rate loan is a loan that has a variable interest rate that changes during the entire tenure of the loan.

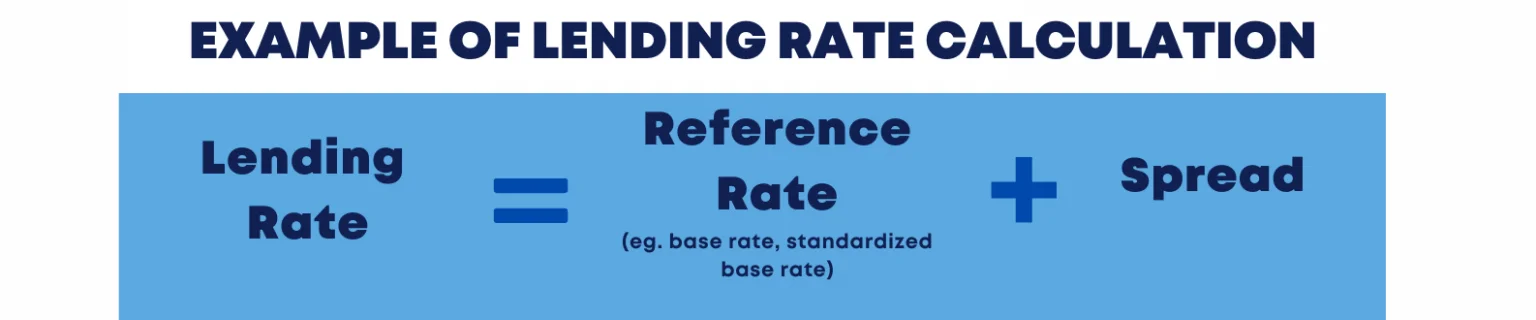

As a borrower, you should know what is the Lending Rate for your floating-rate loan. The Lending Rate is determined by the Reference Rate and Spread. The Lending Rate influences the whole repayment amount of your loan.

The OPR Rises Again! Should You Apply For Fixed Or Floating Rate Loan?

The first component in the Lending Rate is the Reference Rate. This Reference Rate determines the changes in the repayment amount of retail floating-rate loans throughout the loan tenure. There are a few types of Reference Rate such as Base Lending Rate and Base Rate.

i) Base Lending Rate

The Base Lending Rate is determined by the overall financial situation of all the financial institutions in Malaysia. The Overnight Policy Rate (OPR) is used as a benchmark as well as the cost incurred to lend money to the financial institutions.

ii) Base Rate

The Base Rate is determined by financial institutions based on the cost of funds and Statutory Reserve Requirement (SRR) as a benchmark for each bank. The banks in Malaysia are given the freedom to determine their own Base Rate, based on the set formula and Overnight Policy Rate from BNM as a benchmark.

The second component is Spread. The Spread includes the credit risk of the borrower, operational costs, liquidity premium, and profit margin of the banks along with other costs. Usually, the Spread does not change during the duration of your loan. The spread is determined by the banks and each bank has a different spread.

The formula for the latest calculation

Example of Reference Rate Framework before 2015:

Lending Rate (4.7%) = Reference Rate (Base Lending Rate) (6.9%) – Interest Rate (2.2%)

Example of Reference Rate Framework after 2015:

Lending Rate (4.7%) = Reference Rate (Base Rate) (3.5%) + Spread (1.2%)

What is the Revised Reference Rate Framework? What are the differences?

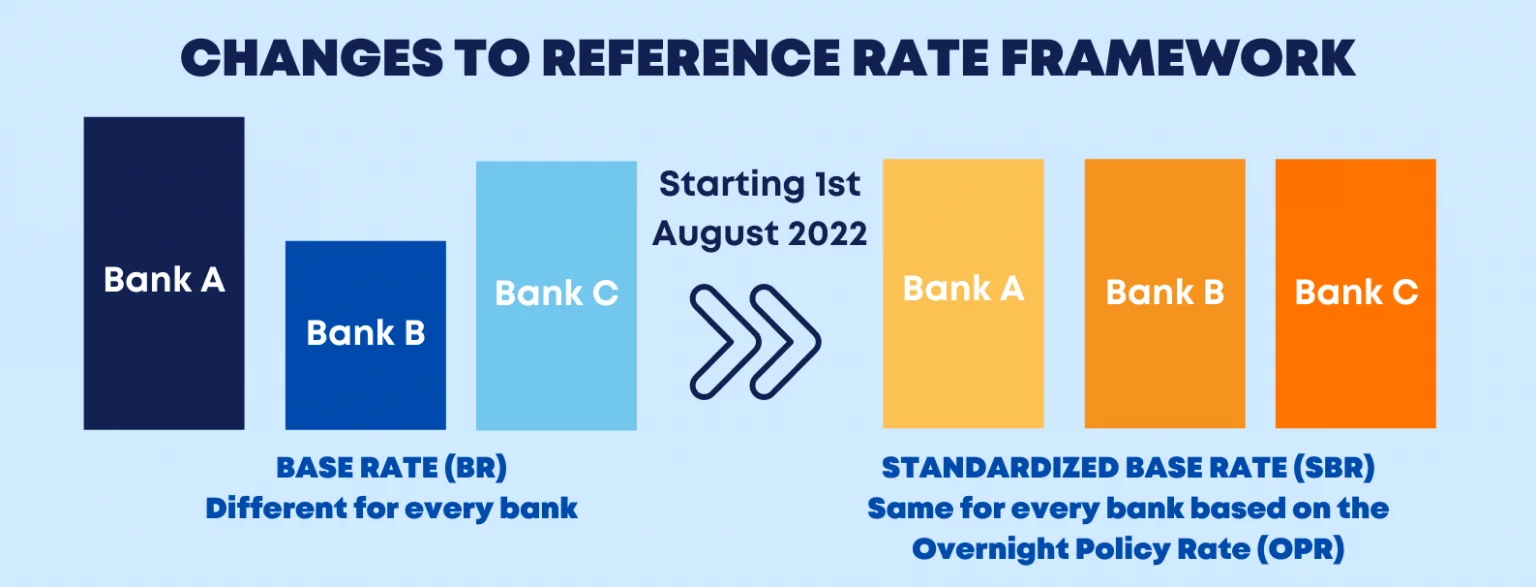

Recently, Bank Negara Malaysia (BNM) has introduced the Revised Reference Rate Framework. Under the Revised Reference Rate Framework, the Standardised Base Rate (SBR) will replace the Base Rate as the reference rate for new retail floating-rate loans. The Revised Reference Rate Framework will be implemented starting from 1st August 2022, next year.

In contrast with the Base Rate, the Standardised Base Rate is in line with the Overnight Policy Rate (OPR) and will be determined by the Monetary Policy Committee of Bank Negara Malaysia. In other words, the Standardised Base Rate will be based on the Overnight Policy Rate. With this, it will be easier for borrowers to make comparisons for retail loan products offered at financial institutions. All of the banks in Malaysia will be using the same Standardised Base Rate determined by BNM. The Standardised Base Rate will determine the Lending Rate for new retail floating-rate loans, refinancing for existing retail loans, and revolving retail loans renewal.

This change enables customers and borrowers to make easier decisions as the Standardised Base Rate is more transparent compared to the previous Base Rate. Governor Datuk Nor Shamsiah also supported this change with a statement that highlights both customers and borrowers will have an easier time understanding the changes in the repayment of their loans as the Standardised Base Rate solely depends on the changes of the Overnight Policy Rate.

Based on the illustration above, the Base Rate will be replaced by the Standardised Base Rate starting from 1st August 2022 with a big difference in the Reference Rate. Before this, the Base Rate is determined by the bank themselves. Hence, each bank has a different Base Rate according to its own benchmark. But, with this new change, all of the banks in Malaysia will have the same Standardised Base Rate.

The standardization of this new Standardised Base Rate will help users and borrowers to make effective comparisons between loans offered by the banks. Users are also able to make more accurate comparisons when applying for retail floating-rate loans.

Even though the Standardised Base Rate is standardised for all of the banks, the Lending Rate and loan approval will still change based on each customer as the spread changes according to individuals and banks as it is based on the credit score of an individual, risk appetite, and business strategy of each bank. Spread will still be maintained, where the components for lending rate such as credit risk of the borrower, operational costs, liquidity risk premium, profit margin, and other costs will be determined by each of the banks.

Understanding The Impact Of Transitioning From Base Rate To Standardised Base Rate

You might have a few questions running in your head “What will happen to my retail floating-rate loan? I just applied this year” “Will the calculation for the lending rate of my floating-rate loan change next year?”

- Retail floating-rate loans before 1st August 2022

The transition from Base Rate to Standardized Base Rate does not affect or give any impact to lending rates for existing retail floating-rate loans. Existing retail floating-rate loans before 1st August 2022 will still be using Base Rate and Base Lending Rate as Reference Rate.

Hence, existing customers and borrowers do not need to worry about the new transition as it will not affect existing retail floating-rate loans and just continue the repayment as per usual.

- New retail floating rate loans (housing loan and personal loan) starting 1st August 2022

Only new retail floating-rate loans such as house loans and personal loan will be using the Standardised Base Rate. This transition will not affect any other fixed rate loans such as car loans (hire purchase) or business loans.

After the effective date, both Base Rate and Base Lending Rate will move exactly with the Standardised Base Rate if there are any changes done to the Standardised Base Rate, the Base Rate, and Base Lending rate will also be adjusted simultaneously.

Hence, all the banks in Malaysia are requested to display the Standardised Base Rate on their website and branches along with the current Base Lending Rate and Base Rate that have been displayed before, for customer’s reference and help them to determine what reasons for applying a personal loan they should apply based on the rate. The banks are given a transition period of one year along with time to make preparations and improve their systems to ensure that the implementation of the Revised Reference Rate Framework will run smoothly.

For a clearer comparison between the Reference Rates, you can refer to the table below:

| Standardised Base Rate | Base Rate | Base Lending Rate | |

| Implementation | Starting 1st August 2022 | 2nd January 2015 | Since 1983 |

| Determined by | By Bank Negara Malaysia based on the Overnight Policy Rate (OPR) | By the bank themselves based on benchmarks such as cost of funds and statutory reserve requirement | By bank themselves based on the cost of lending money to other financial institutions and influenced by Bank Negara Malaysia |

| Changes in rate | In line with Overnight Policy Rate | Bank can adjust the Base Rate even though the Overnight Policy Rate does not changes | Changes according to Overnight Policy Rate |

| Function | More transparent and makes it easier for users to make comparisons | More transparent but it is hard for users to make decisions |

Determines the lending rate but less transparent |

The Differences between Standardised Base Rate, Base Rate and Base Lending Rate

Situation A: You have a floating-rate personal loan amounting to RM10,000 for a tenure of 10 years with Bank A.

| Standardised Base Rate | Base Rate | Base Lending Rate | |

| Reference Rate | 1.75% | 1.85% | 6.8% |

| Spread | 1.7% | 1.60% | 3.35% |

| Lending Rate | 3.45% (1.75% + 1.7%) | 3.45% (1.85% + 1.60%) | 3.45% (6.8% – 3.35%) |

| Monthly Installment | RM112.08 | RM112.08 | RM112.08 |

Based on the calculation above, all of the monthly installment for the three types of reference rate are the same. The difference is at the determination of the reference rate and spread.

Situation B: You want to apply for a floating-rate personal loan amounting to RM150,000 for a tenure of 10 years. You have the choice to go to three different banks. How do you compare the Lending Rate for Bank A, B and C?

| Base Rate | Standardised Base Rate | |||||

| Bank | Bank A | Bank B | Bank C | Bank A | Bank B | Bank C |

| Reference Rate | 1.65% | 1.80% | 1.50% | 1.75% | 1.75% | 1.75% |

| Spread | 1.35% | 1.5% | 1.7% | 1.5% | 1.35% | 1.6% |

| Lending Rate (Reference Rate + Spread) | 3% | 3.3% | 3.2% | 3.25% | 3.1% | 3.35% |

| Monthly Installment | RM1,625 | RM1,662.50 | RM1,650 | RM1,656.25 | RM1,637.50 | RM1,687.50 |

Based on the calculation above, the Base Rate for Bank A, B and C are different because the Base Rate is determined by each bank respectively.

In contrast to the Standardised Base Rate, all of three banks have the same rate at 1.75%. The difference is at the spread as it is determined by each bank separately. Although the Standardised Base Rate is the same for Bank A, B and C, the spread is what makes the differences in the Lending Rate.

When the Reference Rate or the Standardised Base Rate is the same for each bank, it is easier for customers to make decisions and more accurate considerations to apply for retail floating-rate loans.

If you want to apply for retail floating-rate loans after 1st August 2022, you can make a more accurate comparisons after the Revised Reference Rate Framework is implemented.

Direct Lending’s Opinion

As a personal lending platform that offers safe and affordable personal loan to borrowers, we also would like to offer some useful advice to our users. Direct Lending will not be affected by the transition of Base Rate to Standardised Base Rate because as of now the loan products offered at Direct Lending are all fixed rate loans. Hence, users and customers of Direct Lending that has successfully receive the personal loan financing do not need to worry about this transition at all.

For users or borrowers who are interested to apply for retail floating-rate loans in the future or starting from 1st August 2022, ensure that you check the interest rate offered by the bank. You can check the interest rates easily through their websites.

What do you need to do if you want to apply for retail floating-rate loan starting 1st August 2022?

- Make comparisons based on the lending rate or spread offered by the different banks before making the decision to apply for a new loan.

- Ensure that you read the product disclosure sheet to know about the important and accurate information regarding the financial product offered by different banks.

- Identify the Lending Rate and the amount of loan repayment for different banks.

- Understand that the loan repayment for floating-rate will change in the future based on the Overnight Policy Rate.

- Assess if you are able to make repayments for your loan if the Lending Rate increases in the future.

- Choose a loan that best suits you based on the comparison of the products offered by the banks.

In conclusion, the transition from Base Rate to Standardised Base Rate will help users to make more accurate decisions and comparisons for retail floating-rate loans offered by the banks. This transition will also encourage for banks to compete healthily in offering interesting products in the market.

This article is prepared by Direct Lending a personal lending platform that helps you to find, compare and apply for the best suited personal loan for you. Our smart eligibility checking system is able to recommend the best bank and koperasi personal loan for you.

Our service is 100% free, no upfront charges and processing fees.

{kind=link}

{kind=link}