Is Licensed Moneylender Considered an ‘Ah Long’?

The recent case of loan sharks charging RM500 for every 30 minutes delay in repayment is not an exaggeration. This case happened to an insurance agent who borrowed RM3,000 and paid the full amount. But, the loan shark demanded RM1,500 as charges for his late payment. The loan shark also threatened the borrower that he will cause injuries to the borrower and his family. Situations as such are ridiculous but true. This has stirred confusion among the general public which backlash towards licensed moneylender as well.

This has caused a lot of confusion and blurred the line between a licensed moneylender and Ah Loong even more. People find it hard to trust licensed moneylenders, in fear that they are actually Ah Long that is trying to trick them. Such situation has created a taboo in our society regarding licensed moneylender and leads to various negative connotation. This article is written in hope to help people to be able to distinguish between licensed moneylender and Ah Long.

Table of contents

- Licensed Moneylenders vs. Ah Long

- Pros of Personal Loan From Licensed Moneylenders

- Cons of Personal Loan From Licensed Moneylender

- Tips to Protect Yourself from Ah Long

- Example of Loan Agreement Contract For Licensed Moneylender Loan (Jadual J KPKT)

- Video: Licensed Moneylenders VS Ah Long VS Loan Scammers

- Summary

Licensed Moneylenders vs. Ah Long

Many are confused with the general misconception that all moneylenders are ‘Ah Longs’ or loan sharks, who charge high-interest rate. In fact, there are legal moneylenders who are regulated by the government, more specifically by The Ministry of Housing and Local Government (KPKT). KPKT recently launched an initiative to rebrand registered licensed moneylenders as the ‘Credit Community’ with the purpose of changing the general public’s perception and exposure towards safe lending facilities.

Please note that money lending is not governed by Bank Negara. In case, a claimed licensed moneylender shows you a license by Bank Negara, it is most likely a fake license. Below is an example of a fake license.

Today we would like to expose the differences between ‘Ah Longs’ and Licensed Moneylender who follows the regulations, the Moneylenders Act 1951 (MA). The table below depicts the differences.

| LOAN SHARK / AH LONG | CRITERIA | LICENSED MONEYLENDER WHO COMPLIES WITH MONEYLENDERS ACT 1951 |

| No one but themselves. They set their own rules. | Governed and Regulated By | Ministry of Housing and Local Government (KPKT). |

| Not licensed. Again, they set their own rules. | Licensing | Section 5(2) of MA requires them to apply licensing every 2 years. |

| Usually it is ‘sepuluh-tiga’ which comprises of 30% interest charged monthly. But they can also charge you as they like. | Interest Rate | Maximum 12% p.a (secured loans) and 18% p.a (unsecured loans). |

| There might be other hidden costs that they will set up as they like. | Other Charges | It consists of attestation and lawyer fees, credit check fees and stamp duty. |

| No loan agreement involved. | Loan Agreement | The loan agreement will be validated by a third party i.e. Lawyer, Legal Officer, Commissioner for Oaths. |

| It is unregulated and they advertise whatever they like. | Advertising | Under Section 11 of MA, they must apply permit for advertisements. Under Section 27A of MA, they are prohibited from employing agents or canvassers. |

| They will hold your personal belongings like IC, passport, bank cards, etc. as security deposit. | How to Apply | The standard loan documentation process involves a background check on documents like IC copy, salary slip, bank statement, EPF, etc. |

| Examples of extortion activities include splashing red paint, harassing and threatening to hurt the borrower’s family members. | How to Chase Bad Debt | They send reminders, hire debt collectors, issue letter of demand, set blacklist on CCRIS and CTOS or offer AKPK counselling services. |

| They charge whatever they like. | Charges for Late Payment | The charges are between 3-5% for late payment. |

| Borrowers are not allowed to make an early loan settlement because it does not bring profit to them. | Early Loan Settlement | Yes, they allow early loan settlement. |

| Accept all kind of borrower, even borrower with negative and ‘blacklisted’ record. | Borrower’s Credit Eligibility Criteria | Depends on the lender, some accept negative CTOS record, high outside commitment, ‘Special Attention Account (SAA)’in CCRIS, registered with AKPK. |

| Have no maximum limit for loan | Loan Sum | Generally starts from RM1,000 to RM10,000. |

| All individual are eligible for loan application | Eligibility | Civil servant, private sector worker and self-employed individual and must have a payslip/ statement. |

| No reports were submitted to KPKT | Annual Transaction Records |

Reports need to be submitted to KPKT. |

Not to forget, here are some extra tips to shield yourself from dealing with an ‘Ah Long’. Better safe than sorry!

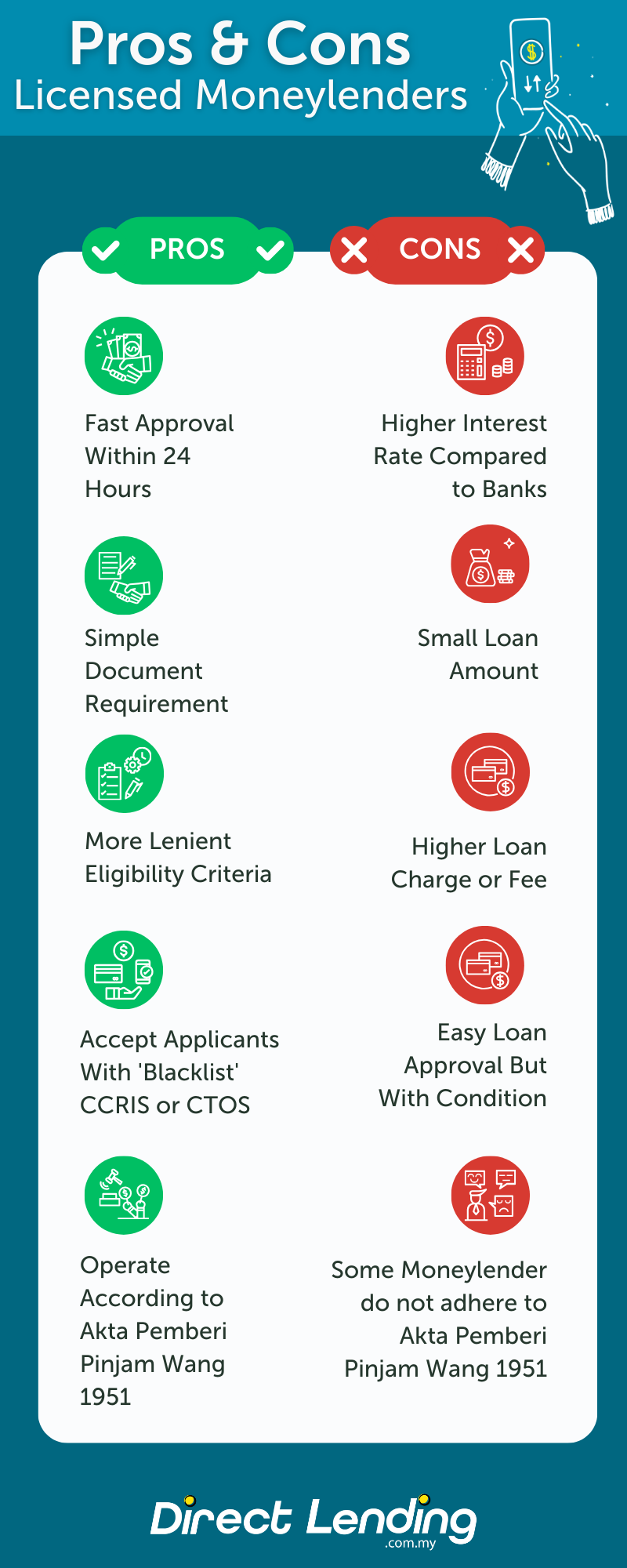

Pros of Personal Loan From Licensed Moneylenders

- Fast Approval Within 24 Hours - Most Licensed moneylender guaranteed financing as fast as 1 working day, provided that every documents prepared by applicants are legitimate and complete.

- Easy Document Requirement - Applicants only need to prepare basic documents such as IC copy, payslip, bank statement and utility bills only.

- Eligibility Criteria Is Less Strict - Applicants with minimum income of RM1,500 and employment period of at least 3 months are eligible to apply.

- Accept Applicants With Blacklist, CCRIS or CTOS Problem - Most loan applications with bad credit record such as poor CCRIS, CTOS or even blacklist will be rejected by the bank. As such, these applicants can still apply financing with licensed moneylenders

- Operate According to Malaysian Legislation (Akta Pemberi Pinjam Wang 1951) - All licensed moneylender companies need to comply with the law by KPKT authority and operate by the procedures set by the act of Akta Pemberi Pinjam Wang 1951. For example, they are prohibited to hold ATM bank cards and the interest rate should not be more than 1.5% per month or 18% per annum.

Cons of Personal Loan From Licensed Moneylender

- Higher Interest Rate Compared to Banks - Licensed moneylender or credit community companies are private companies, which differs from large financial institutions like banks. Therefore, the interest rates they impose are higher than banks.

- Small Loan Amount - Due to the high interest rates, legitimate licensed money lending companies typically do not want to take on high risks such as providing large amounts of financing. Some of these licensed money lending companies also do not have large funds like conventional banks.

- Higher Loan Fees - There are several loan fees that will be deducted from the loan amount. These loan fees are usually higher compared to the fees charged by banks.

- Loan Approval Depends on Lender's Terms - There are several approval conditions for applicants with 'blacklisted' issues in CCRIS and CTOS. The lender may impose stricter conditions in approving the loan amount.

- Some Credit Community Companies Do Not Comply with the Moneylenders Act 1951 - There are reports finding that credit community companies operate similarly to illegal moneylenders or loan sharks. So, you need to be careful in choosing a money lending company before dealing with them.

Tips to Protect Yourself from Ah Long

Tip 1: Check the company’s SSM number on the KPKT website

Tip 2: Check if they display their licensing at their office issued by KPKT, not BNM

Tip 3: Ensure that the loan offered by the lenders are in compliance with the Moneylenders Act 1951, particularly the interest rate is not above 18% per annum and the loan agreement is valid with proper loan documentation in place

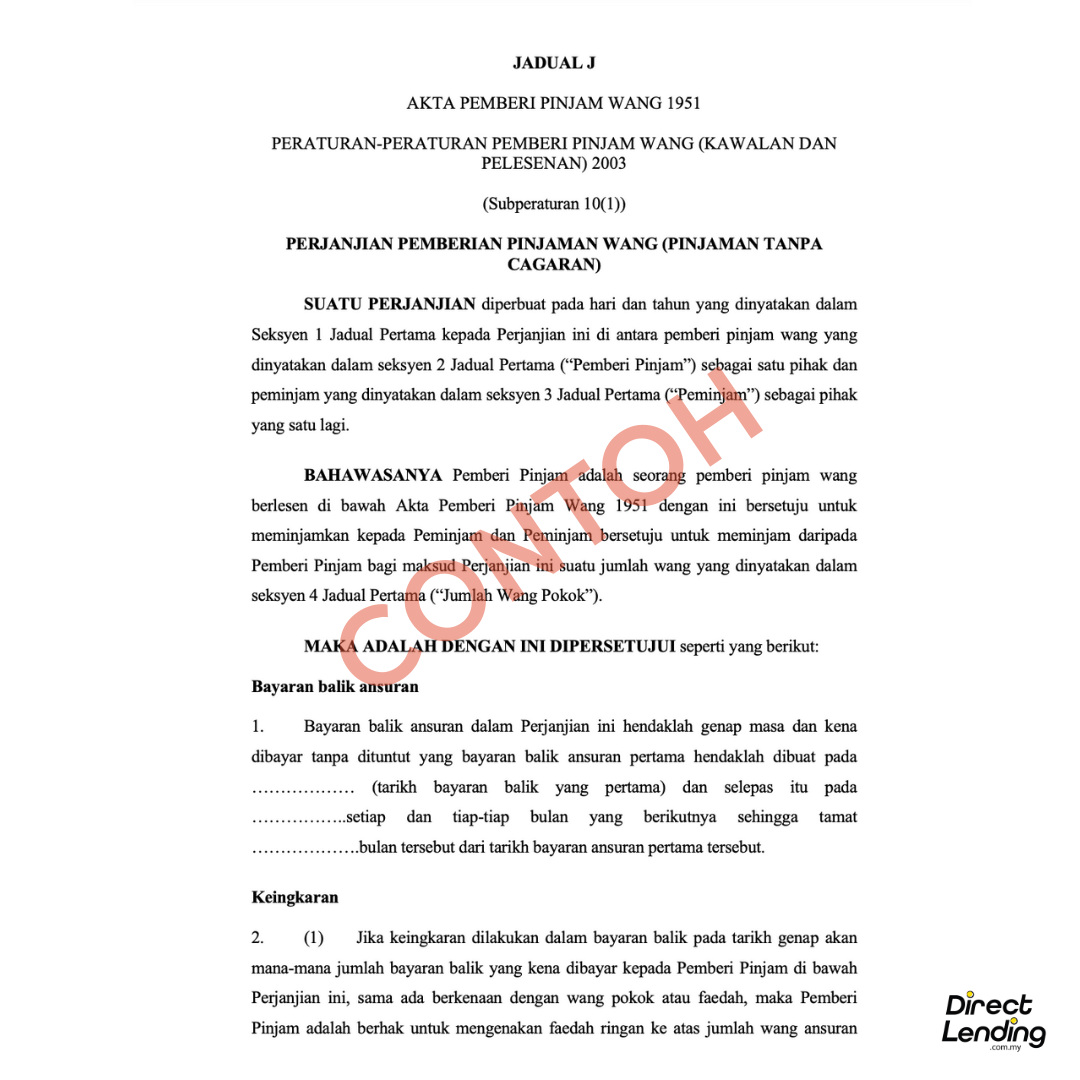

Example of Loan Agreement Contract For Licensed Moneylender Loan (Jadual J KPKT)

There are a lot of ways to identify trusted money lender and credit community companies in Malaysia. Other than checking the license status of the money lending company through iKredikom, you can also observe the loan procedure conducted.

Trusted money lender will never ask to hold your ATM card or online banking password. These practices are against the law enacted according to Moneylenders Act 1951 (Akta Pemberi Pinjam Wang 1951). Moreover, a trusted money lender will only use a legitimate loan agreement contract which is Borang Jadual J KPKT for the loan process. You can see the example of the legitimate loan agreement contract below.

Video: Licensed Moneylenders VS Ah Long VS Loan Scammers

Summary

Only apply for a loan with a financial institution that you trust. The best way is of course to obtain a loan from banks. However, banks can be pretty strict when it comes to their loan requirements especially with credit score. The best ways on how to improve your credit scoring are highlighted in our article.

Most people who falls victim to Ah Long are people who are in a desperate need of money. Being in a rough financial situation, sweet and soothing words from Ah Long sure sound much more enticing than one can imagine. It is totally understandable that you have your own reason as to why you would apply for personal loan, just be sure to make one with licensed moneylender.

In general, if you are eligible for bank loan, it should be you main option as it offers lower interest rate. If you are not eligible, it is better for you to look for trusted licensed moneylender like credit community loan and bank loan and koperasi. Eventhough the loan process with Ah Long is as easy as a breeze, you should think about the long aftereffect of being trapped with ridiculous agreement and rule that Ah Long made up.

In case you are low income or do not have a credit score, you still have an option to obtain a safe loan from co-operative (koperasi), yayasan or licensed moneylenders that are reputable and legal. If you are in need of financing, check your loan eligibility for free with Direct Lending, an online personal lending platform that work with only reputable and licensed lenders.

This article is written by Direct Lending – An online personal lending platform that provides bank and koperasi personal loan as well as licensed moneylenders personal loan. We can help you find, compare and apply personal loan that best suits your financial needs. Check your eligibility for free, no upfront payment or processing fees and get a loan rates from 2.95% p.a. or 2 working days.

{kind=link}

{kind=link}

{kind=link}